Investment Update June 2026

- ABP Team

- Jun 3

- 5 min read

Updated: Jun 10

Key Highlights: • The S&P 500 rose 5.15% in May, while the Nasdaq gained 10.49%, despite heightened geopolitical tensions in the Middle East and rising crude oil prices.

• The tentative US-Iran ceasefire became the key macro driver during May, with its durability expected to shape market direction over the coming quarter.

• WTI oil ended near $87, remaining above the $65 pre-conflict level but below the $96 to $100 peak reached during the crisis.

• A sustained ceasefire and oil prices falling toward $70 could ease inflationary pressures and reopen the possibility of Federal Reserve rate cuts.

• A breakdown in the ceasefire and oil prices rising toward $110 to $120 could significantly increase inflation and create a difficult policy environment for central banks.

• At portfolio level, positioning benefited from strong equity markets, short-duration bonds, hard asset allocations, and absolute return strategies, supporting performance and risk management.

• The S&P 500 closed near record highs around 7,580, supported primarily by strong corporate earnings and continued AI-driven investment.

• Morgan Stanley’s expectation of 23% EPS growth in 2026 continued to gain support, while annual AI capex investment approached $500 billion.

• AI-related equities continued to outperform broader markets, reinforcing the concentration of market leadership within mega-cap technology companies.

The old stock market saying, “sell in May and go away,” has now been proven wrong for four consecutive years. The S&P 500 rose by 5.15% in May this year, while the Nasdaq gained 10.49%, despite a Middle East crisis involving the world’s largest superpower and a spike in crude oil prices. There must be more to it. Indeed, there is, and we unpack the key details in the Investment Update that follows.

The most consequential macro variable in May was the tentative US-Iran ceasefire, and its durability will shape the next quarter. WTI oil ended near $87, above the $65 pre-conflict level but below the $96 to $100 peak, leaving a geopolitical premium of about $15 to $20 per barrel. If the ceasefire holds, oil falling toward $70 would ease inflation and reopen Fed flexibility for a rate cut. If it breaks down and WTI oil moves to $110 to $120, inflation will rise further and create a clear policy dilemma. Strength in gold and silver suggests this risk remains unresolved, and our commodity overweight reflects that uncertainty.

In America, the S&P 500 vaulted to record highs during May, closing near 7,580, a remarkable outcome given the macro backdrop. The justification lies in earnings. Morgan Stanley’s estimate of 23% EPS growth in 2026 is being broadly vindicated, with AI capex investment running at nearly $500bn annually, providing a structural demand floor for the mega-cap technology firms.

The chart shows resounding strength in AI stocks.

However, the consensus narrative is now being tested. The index has re-rated to levels where further multiple expansion requires either a Fed pivot, which is unlikely, or an acceleration in earnings that would need to broaden beyond AI-adjacent names. The final day of May saw unusually large out-of-the-money call option activity for August 2026, contributing to the implied volatility up, index up dynamic currently evident across US equities. This type of environment typically precedes sharp market moves.

US Treasuries experienced renewed volatility during May 2026, with long-end yields pushing higher as markets adjusted to persistent inflation pressures with CPI printing at 3.8% and a resilient growth outlook. The 30-year yield moved closer to the 5% threshold, reflecting increased term premium and heavy issuance expectations, while shorter maturities remained anchored by a Federal Reserve that signalled no near-term policy pivot. The move resulted in a modest steepening of the yield curve and created tighter financial conditions, with higher real yields beginning to challenge equity valuations and broader risk assets.

We note the arrival of a new Federal Reserve Chair, Mr Kevin Warsh, and we expect to discuss early impressions here next month.

Meanwhile in Japan, the Bank of Japan faces a classic open economy trilemma. Maintaining yield curve control to support bond markets, conflicts directly with the inflationary pass-through from a weak yen, while tightening policy to defend the currency risks destabilising the world’s largest government bond market and triggering a global carry trade unwind. Japanese CPI inflation has remained above 2%, driven domestically for the first time in decades, giving the BoJ genuine justification to normalise policy. However, the pace of adjustment is critical, as any abrupt move risks a disorderly unwind of the yen carry trade, which remains one of the largest and most embedded positions in global macro. We are watching the June BoJ meeting as a potential inflection point.

China’s equity markets were mixed during May, as weak domestic demand and ongoing property sector stress offset targeted policy support from Beijing. Authorities continued to signal incremental stimulus focused on infrastructure and technology investment, but investors remained cautious given subdued consumer confidence and uneven credit growth. While select sectors linked to advanced manufacturing and exports showed resilience, broader indices struggled to sustain momentum, reflecting lingering concerns about structural growth challenges and the limited scale of policy easing so far.

European equity markets delivered modest gains in May, supported by resilient corporate earnings and improving sentiment around industrial and defence sectors. The STOXX Europe 600 edged higher despite ongoing concerns around slow economic growth and mixed data from Germany and France. Inflation, provoked by the Hormuz crisis and Europe’s critical dependency on energy, that had pushed higher the previous month, began to moderate in May. However, upside remained constrained by weak consumer demand, political uncertainties, and sensitivity to higher global bond yields.

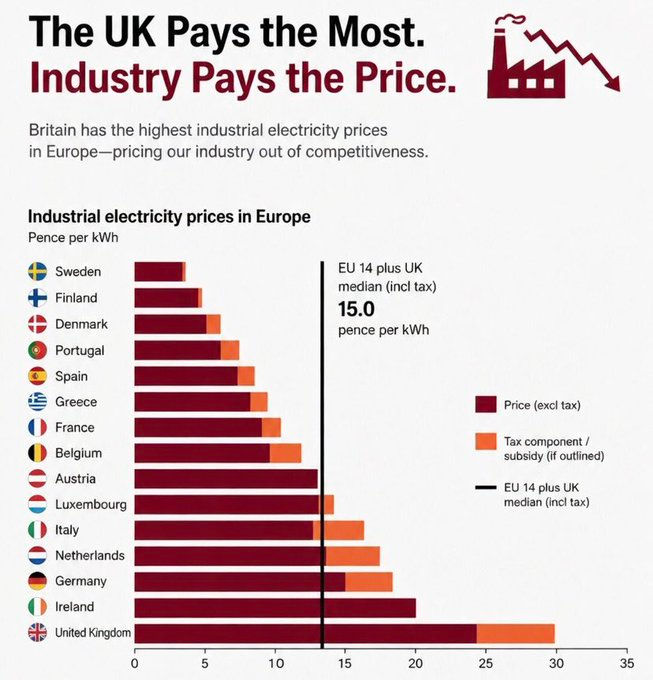

The price of energy is highest in the UK. This is hurting industry as it competes with Europe, and beyond.

UK equity markets delivered modest gains in May, supported by strength in energy, mining and defensive sectors, which benefited from elevated commodity prices and global uncertainty. The FTSE 100 outperformed more domestically focused indices, as the FTSE 250 remained constrained by weak UK growth and cautious consumer sentiment. Inflation showed gradual signs of easing, but remained above target, leaving the Bank of England in a restrictive stance. UK Gilt markets saw some disruption due to debt levels rising to £2.9 trillion under Chancellor Reeves, whilst output and GDP fell. Political theatre within the governing party adds to the weakness. Overall, the market continued to reflect a mix of global tailwinds and domestic economic and political challenges.

At portfolio level, the buoyancy of equity markets served us well. Likewise, our positioning in high-quality, short-duration bonds proved sensible. A lower fixed income weighting, combined with an allocation to hard assets such as gold and silver, is proving effective. Exposure to absolute return strategies has also helped deliver asymmetrical returns, cushioning downside while capturing attractive upside. As we approach the halfway point of 2026, we are pleased with portfolio performance and risk management to date and remain focused and vigilant from here.

Written by the Alpha Beta Partners Investment Team.

All sources Bloomberg unless otherwise stated.