Fertiliser Shock and the Food Price Pipeline

- Andrew Thompson

- Apr 28

- 3 min read

Updated: Apr 29

Whether you are a fan of Clarkson’s Farm or not, it has been hard to escape the news coverage highlighting the tough times faced by British farmers in recent years. The war in Iran has created significant delays in fertilisers reaching the world’s major growing regions. This gap between delivery and planting could see a food inflation problem quietly incubating across the globe.

A disruption at the Strait of Hormuz has far wider consequences than energy markets alone, and one of the most significant spillovers is through fertiliser prices and ultimately global food costs. As fertiliser markets tighten and prices rise, the effects on agriculture unfold gradually but can be powerful and persistent.

The Hormuz Strait is a critical chokepoint for global trade in both fertilisers and the raw inputs used to produce them. Large volumes of ammonia, urea and phosphate fertilisers pass through the region, while natural gas exports from the Middle East underpin nitrogen fertiliser production worldwide. A blockage or sustained disruption raises prices through a combination of restricted physical supply, higher shipping and insurance costs, and precautionary buying by importers concerned about future shortages.

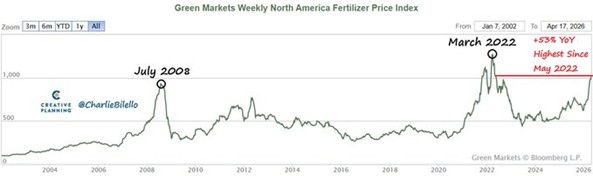

About a third of global fertiliser supply passes through the Strait of Hormuz. Delays reaching the growing regions will likely see food prices rise.

Farmers feel the impact almost immediately in input markets. Fertiliser typically represents one of the largest variable costs in crop production, particularly for cereals. When prices spike, growers face a difficult trade-off between absorbing higher costs, reducing application rates, or switching crops. In many cases, fertiliser demand is postponed rather than eliminated at first, which creates a lag before the effects appear in food markets.

The delay between fertiliser price shocks and food inflation is usually one to three growing seasons. In the near term, existing fertiliser inventories and pre purchased contracts soften the blow, as does margin compression. Crops already planted are unlikely to see major changes in nutrient application. Over time, however, persistently high prices lead farmers to apply less fertiliser or plant fewer hectares of nutrient intensive crops. Lower yields then show up at harvest, tightening supply and pushing prices higher at the wholesale level. Retail food prices often rise later still, sometimes twelve to eighteen months after the initial disruption.

Staple grains are the most exposed commodities. Wheat, maize and rice depend heavily on nitrogen fertilisers, and even modest reductions in application can materially reduce yields. Maize is particularly vulnerable, as it has one of the highest nutrient requirements of any major crop and is widely grown in fertiliser intensive systems. In regions where farmers are already operating on thin margins, reduced fertiliser use may also lead to poorer grain quality, compounding supply issues. Orange juice is another commodity potentially impacted.

Oilseeds such as rapeseed, sunflower and soybeans are also affected, though to varying degrees.

Soybeans benefit from nitrogen fixation, which offers some insulation from fertiliser shocks. That said, phosphorus and potassium remain critical, and shortages or higher prices of these inputs still raise production costs. Edible oil prices can therefore experience upward pressure, especially if farmers shift acreage away from oilseeds toward less input dependent crops.

The knock-on effects extend through the food system. Higher grain and oilseed prices increase animal feed costs, which then filter into meat, poultry, egg and dairy prices. This secondary wave of food inflation tends to occur with an additional lag, meaning consumers may feel the impact over several years rather than months. Past fertiliser price shocks show that protein prices can remain elevated long after crop prices peak.

Developing economies are typically hit hardest. Farmers in lower income regions are more sensitive to fertiliser prices and less able to absorb cost increases. Reduced usage can lead to sharper yield declines, intensifying food insecurity and increasing reliance on imports at precisely the moment global prices are rising.

In summary, a Hormuz related fertiliser shock would not trigger an immediate surge in supermarket prices, but it would plant the seeds for sustained food inflation. If the disruption is prolonged, the largest and most durable impacts would be felt in staple grains and protein markets, with consequences that extend well beyond the original geopolitical event.

The investment opportunity has not been lost on Alpha Beta’s investment team, nor on others across the industry. However, gaining exposure to this theme requires skill and diligence, as investing in commodities is an area best left to professionals.